The £12.3 billion cost of delaying estate planning

Affluent families who delay estate planning could miss out on chances to reduce a potential Inheritance Tax (IHT) bill and pass more on to their families. Find out if you could benefit from considering IHT and how you might pass on assets tax-efficiently.

According to a report covered by Today’s Wills and Probate (5 June 2026), delays in estate planning could cost UK families £12.3 billion when changes mean pensions will form part of your estate next year.

Under the current rules, most pension wealth sits outside your estate for IHT purposes. This made pensions a useful way to pass on wealth. However, for many pension holders, that will change on 6 April 2027, as most pensions will be included in IHT calculations.

However, the new pension rules don’t account for all potential IHT savings. Indeed, £7.9 billion of the total sum is attributed to delaying estate planning.

The report states that a person beginning estate planning at 50 and making use of multiple strategies, such as exemptions, reliefs, and business relief investments, could, on average, pass on £397,000 more to loved ones than those who delayed estate planning until they were 70.

1 in 5 homeowners could be overlooking a potential Inheritance Tax bill

There are many reasons why families delay estate planning

It might seem like something you don’t need to worry about until later in life, or you may mistakenly believe your estate will not be liable for IHT when you pass away.

Yet, you could be closer to the IHT threshold than you think. According to an article in MoneyAge (16 June 2026), a study of homeowners aged 45 and over found that 1 in 5 people with estates worth more than £1 million describe themselves as “just getting by”.

In 2026/27, the nil-rate band is £325,000. If the total value of your estate is below this threshold, no IHT will be due. In many cases, if you leave your main home to a direct descendant, you can also use the residence nil-rate band, which is £175,000 in 2026/27.

You may pass unused allowances to your spouse or civil partner. As a result, you might be able to pass on up to £1 million before IHT is applied to your estate.

That might seem like a significant amount. However, your estate covers your assets, such as your home, investments, and personal possessions, as well as your pension from 6 April 2027. So, it is possible to unexpectedly leave your loved ones with an IHT bill.

Estate planning isn’t just about IHT either. It includes setting out how you want to pass on your assets so they go to your intended beneficiaries, as well as planning for your security later in life. So, even if your estate won’t be liable for IHT, you could still benefit from an estate plan.

4 gifting allowances that could reduce your estate’s Inheritance Tax bill

Gifting assets during your lifetime could reduce a potential IHT bill. However, it’s not as straightforward as simply transferring assets to your loved ones.

First, it’s important to be aware of how a gift could affect your long-term financial security. A financial plan could help you assess the potential impact.

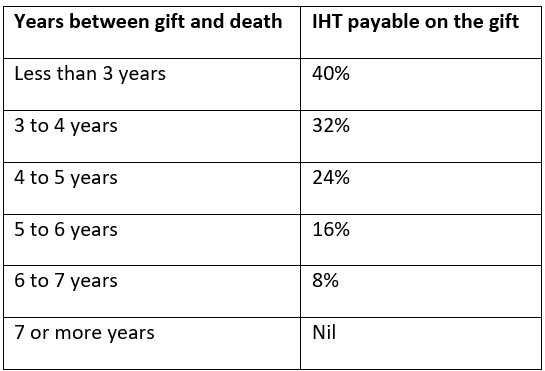

Second, not all gifts are immediately excluded from your estate for IHT purposes. Some may be included in your estate and subject to a tapered IHT rate should the value of all your assets exceed IHT thresholds.

Using these four gifting allowances as part of your wider estate plan could provide a tax-efficient way to pass on assets.

- Annual exemption

The annual exemption allows you to give away up to £3,000 each tax year without the value being added to your estate when calculating IHT. You may gift this sum to one person or split it between several people. You can carry forward any unused annual exemption for one tax year.

- Small gift allowance

Small gifts valued up to £250 can be given to as many people as you’d like each tax year, so long as you have not used another allowance on the same person.

- Wedding and civil partnership gifts

Celebrating a wedding or civil partnership also presents an opportunity to gift tax-effectively. You can gift £1,000 to the happy couple, and the gift will immediately fall outside your estate. This allowance rises to £2,500 for your grandchild or great-grandchild and £5,000 for your child.

- Regular gifts from your income

Regular payments you make to another person can fall outside your estate, so long as:

- There is an established pattern of making these payments

- The payments are made from your regular monthly income

- You can maintain your usual standard of living after making the payments.

This could provide a valuable way to support your family while reducing a potential IHT bill. For example, you might use this allowance to:

- Pay the rent or mortgage for your child

- Contribute to a savings account for your grandchild

- Provide cash to a family member that they can use for living costs.

For this allowance to be applied to your estate when calculating IHT, there needs to be a pattern of making these payments. So, it’s important to keep accurate, clear records of these gifts.

Contact us

If you’d like to understand whether your estate could be liable for IHT when you pass away, and how you might mitigate a potential bill, please get in touch.

Please note: This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

The Financial Conduct Authority does not regulate estate planning or Inheritance Tax planning.

Remember that taper relief only applies to gifts in excess of the nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief.

Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.